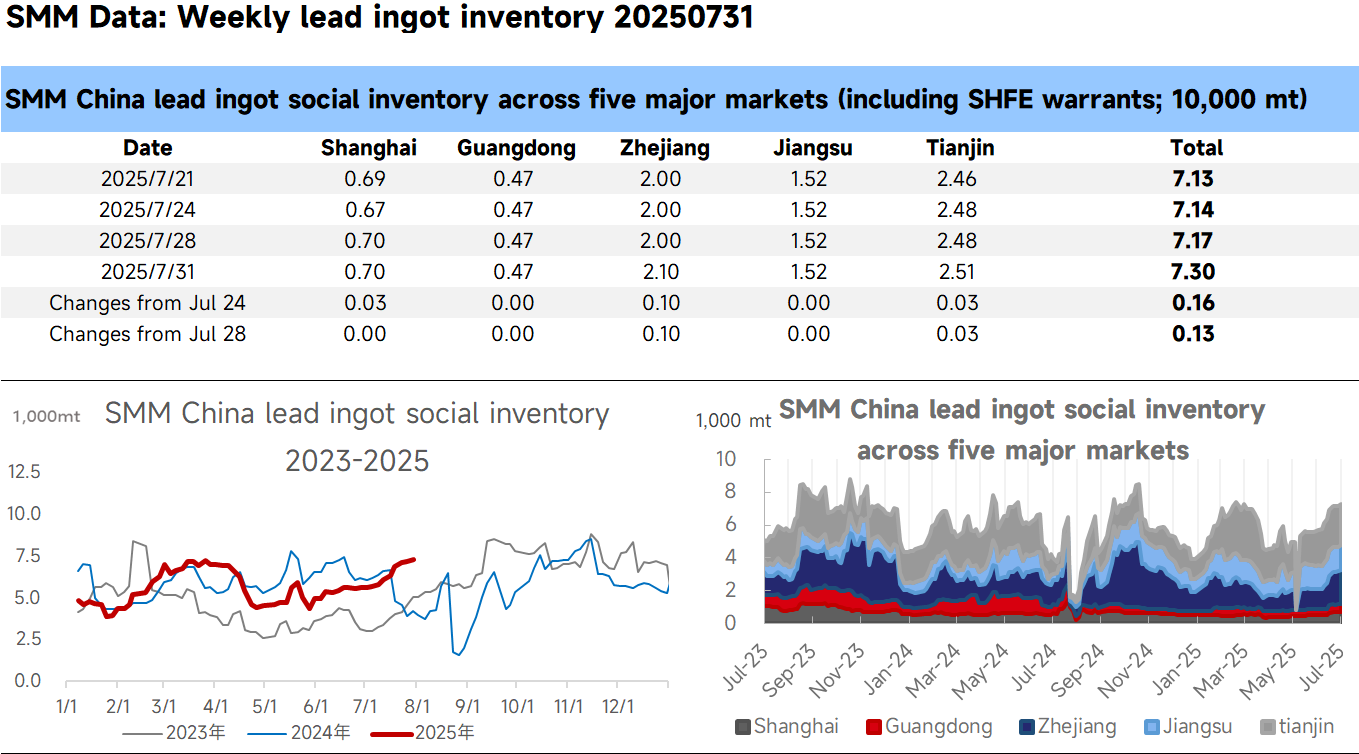

SMM News on July 31: According to SMM, as of July 31, the total social inventory of lead ingots in five regions tracked by SMM reached 73,000 mt, an increase of 1,600 mt from July 24 and 1,300 mt from July 28.

This week, production at primary lead smelters gradually resumed, coupled with the resumption of production at secondary lead enterprises and the commissioning of new capacity, leading to a phased increase in supply. The available spot cargoes in the market increased significantly WoW. Meanwhile, the premium of spot lead continued to decline. In South China, the quoted price for primary lead dropped from a premium of 50-100 yuan/mt against the SMM #1 lead average price last week to parity against the SMM #1 lead average price this week, and even to a discount of 30-20 yuan/mt through negotiation. In addition, the overall price center of lead moved downward, and the purchasing enthusiasm of downstream enterprises improved relatively in the second half of the week. However, they preferred cargoes self-picked up from production sites of smelters with price advantages. Some suppliers tended to transfer their cargoes to delivery warehouses for hedging, and the social inventory of lead ingots continued to rise.